Scientific Asset Allocation Mitigate Risks and Navigate Cycles

Written by AQUMON Team on 2026-04-16

Q1 2026 Global Financial Market Review

In the first quarter of 2026, global financial markets suffered severe volatility under the dual shocks of escalating geopolitical conflicts and a reversal in monetary policy expectations. In late February, the situation in the Middle East escalated abruptly, with the risk of shipping disruptions in the Strait of Hormuz continuously intensifying. As a critical waterway for 20% of global oil trade, the blockade of the strait directly pushed up international oil prices, with Brent crude briefly breaking above $112 per barrel. The energy supply crisis fueled expectations of a rebound in global inflation, completely disrupting the monetary policy layouts of major central banks and rapidly heightening market fears of “stagflation.”

After a brief rally at the beginning of the year, the U.S. stock market experienced a significant correction in March. The Federal Reserve delivered an unexpectedly hawkish signal at its March policy meeting, keeping the benchmark interest rate unchanged at 3.5%-3.75%, while planning only one rate cut for the full year and pushing back the timeline for the first cut to post-September. Consequently, the yield on the 10-year U.S. Treasury note briefly climbed to 4.42%. Equity markets came under notable pressure, with the S&P 500 index accumulating a 4.63% decline in Q1, and the Nasdaq index dropping 7.11%. Global equity markets saw over $7 trillion in market capitalization evaporate in a single quarter, reflecting a sharp contraction in investor risk appetite.

Looking back at the Hong Kong stock market, the Hang Seng Index (HSI) exhibited a volatile trajectory of “initial gains followed by a retreat” in Q1, cumulatively falling 3.29%. Meanwhile, dragged down by divergent corporate earnings and disruptions from global liquidity factors, the Hang Seng Tech Index plummeted 15.70% for the quarter, posting the worst performance among major global indices. Faced with indiscriminate risk-off selling across global markets, the investment risks of single-market and single-asset exposures were infinitely magnified, once again validating the core value of global diversified allocation in mitigating systemic risks and smoothing portfolio volatility.

Flagship Portfolios Deliver Stable Performance, Navigating Turbulent Cycles

AQUMON’s global asset allocation strategy is built upon Modern Portfolio Theory. Leveraging big data and quantitative algorithms, we generate robust, risk-adjusted long-term returns for our clients. We consistently adhere to the following classic three-step scientific allocation framework:

-

Rigorously select low-correlation global asset classes to build a diversified allocation framework;

-

Screen for high-quality ETFs with ample liquidity, low expense ratios, and minimal tracking errors as the underlying instruments for major asset classes;

-

Dynamically optimize asset allocation weights based on shifts in cross-asset correlations and market conditions.

On top of this model-driven approach, we supplement with strict risk control mechanisms and a full-cycle diversification investment philosophy. This has successfully helped investors effectively hedge against single-market systemic risks in turbulent environments and achieve steady long-term returns.

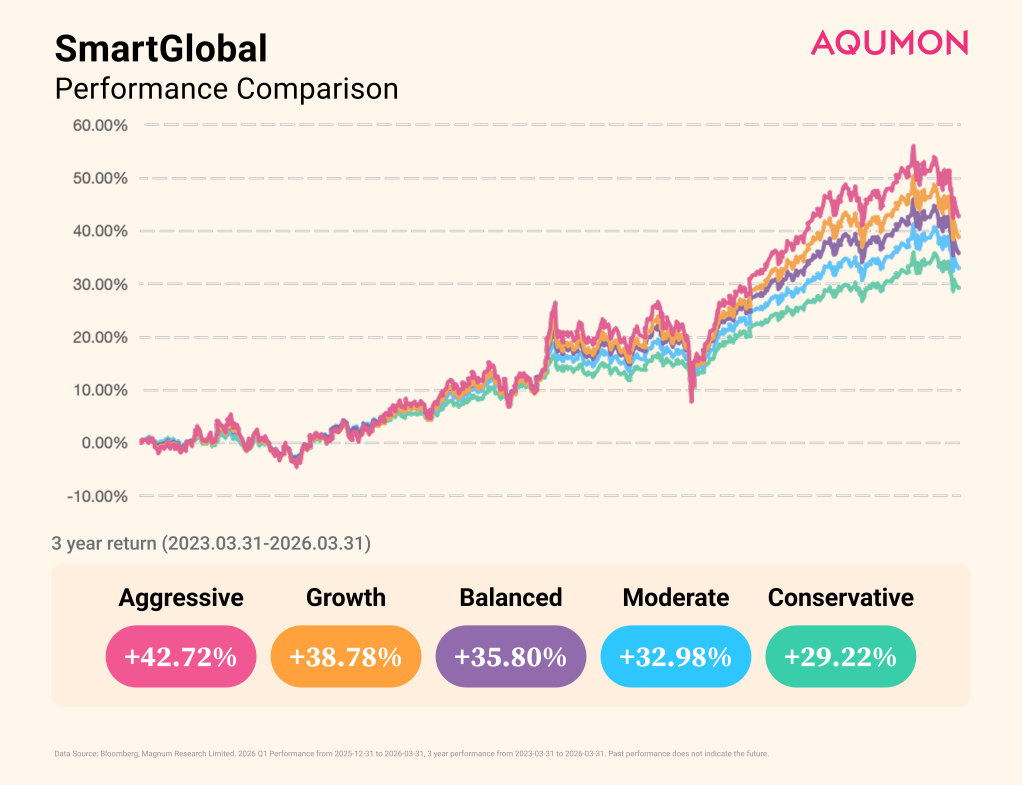

SmartGlobal Series:

In Q1 2026, against the backdrop of a broad market retreat, the SmartGlobal flagship series demonstrated robust resilience. The cumulative returns for the quarter were as follows:

Conservative: -0.93%

Moderate: -1.50%

Balanced: -2.29%

Growth: -2.73%

Aggressive: -3.25%

Over the same period, the cumulative return of the Hang Seng Index was -3.29%. The entire SmartGlobal series outperformed the benchmark index, effectively controlling drawdowns and highlighting exceptional downside protection.

From a three-year cycle perspective (March 31, 2023, to March 31, 2026), the SmartGlobal series consistently delivered outstanding long-term returns:

Aggressive: +42.72%

Growth: +38.78%

Balanced: +35.80%

Moderate: +32.98%

Conservative: +29.22%

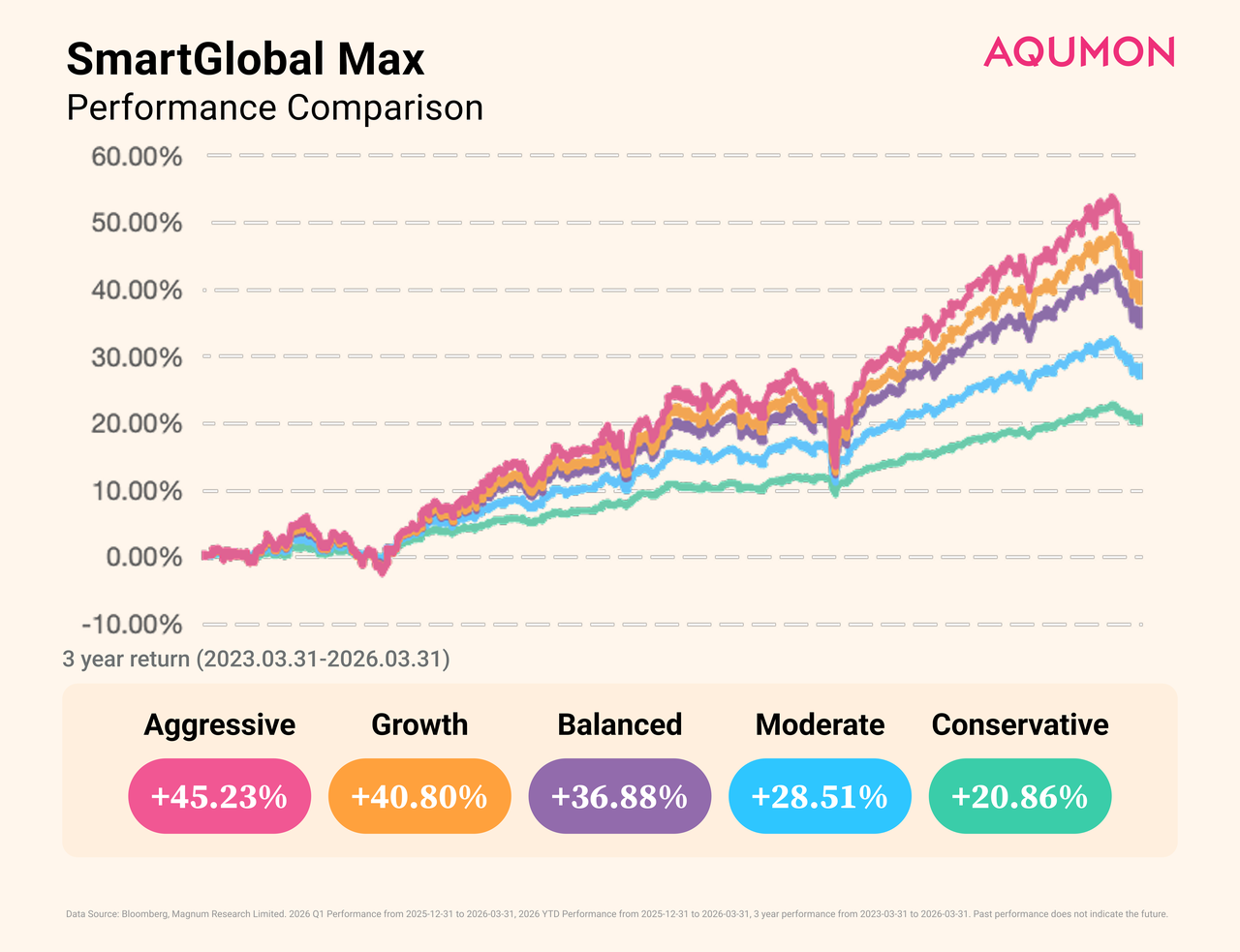

SmartGlobal Max Series:

In Q1 2026, the risk mitigation capabilities of the SmartGlobal Max series were even more pronounced. The cumulative returns for the quarter were as follows:

Conservative: +0.75%

Moderate: +0.10%

Balanced: -0.15%

Growth: -0.25%

Aggressive: -0.45%

Over the same period, the cumulative return of the S&P 500 was -4.63%. The entire SmartGlobalMax series significantly outperformed the benchmark, with the lower-risk tranches even achieving positive returns, reflecting superior risk control.

In terms of long-term performance, the SmartGlobal Max series recorded commendable results over the three-year period:

Aggressive: +45.23%

Growth: +40.80%

Balanced: +36.88%

Moderate: +28.51%

Conservative: +20.86%

Amid intensifying uncertainties in global investing, AQUMON’s flagship series effectively circumvented the systemic risks of single markets, continuing to create long-term value for clients that transcends economic cycles.

Thematic Portfolios Buck the Trend, Demonstrating Ultimate Risk Resilience

In an environment where global markets broadly declined in Q1, AQUMON’s thematic investment portfolios successfully captured scarce structural opportunities and achieved contrarian growth. This was made possible through precise sector selection, strict risk control on underlying assets, and in-depth fundamental research, fully validating their ability to generate alpha and mitigate risks.

Hong Kong Stock Thematic Portfolios:

Despite the weak market conditions where the HSI fell 3.29% and the Hang Seng Tech Index plunged 15.70% in Q1, the Hong Kong stock thematic portfolios moved against the tide, showcasing strong resilience and defensive attributes.

"High Dividends" Portfolio: Focusing on high-quality high-dividend Hong Kong stocks, it recorded a positive return of +8.03% for the quarter, achieving an excess return of over 11 percentage points relative to the HSI.

"Great China ESG" Portfolio: Delivered a Q1 return of +5.01%, also significantly outperforming the broader Hong Kong market, fully reflecting its downside protection and stock-picking logic.

U.S. Stock Thematic Portfolios:

Amidst the volatile market where the S&P 500 fell 4.63% and the Nasdaq dropped 7.11% in Q1, our U.S. stock thematic portfolios also exhibited notable risk resilience:

“Business Winners” Portfolio: Focusing on high-quality U.S. enterprises with long-term economic moats, it achieved a positive return of +2.89% for the quarter, realizing contrarian growth.

“Profit Makers” Portfolio: Experienced a marginal dip of -0.02% for the quarter, almost completely hedging against the systemic downside risk of the U.S. equity market.

“US Market Leaders” Portfolio: Declined by -4.08% for the quarter, but this was still significantly less than the drops of the S&P 500 and Nasdaq indices during the same period, effectively controlling drawdowns.

Q2 2026 Market Outlook

Entering the second quarter of 2026, global markets will continue to face a complex interplay of geopolitical uncertainties, fluctuating inflation risks, and monetary policy tug-of-wars. Market volatility is expected to remain elevated, making scientific diversification the core strategy for navigating market cycles.

We recommend that investors:

Avoid concentrated positions in single markets or single assets;

Diversify geopolitical black swan risks through global, multi-asset allocation;

Increase allocations to high-rated U.S. bonds, using stable coupon income to hedge against equity market volatility.

Regarding Hong Kong stocks, the HSI valuation currently remains in a historically low range, offering excellent allocation value. We suggest moderately increasing allocations to high-quality Hong Kong assets to diversify overseas market volatility risks while seizing potential opportunities for valuation repair.

In turbulent times, an absolute “safe haven” may be hard to find, but scientific asset allocation remains a powerful weapon to mitigate risks and navigate cycles. Supported by big data and quantitative models, AQUMON will continue to build optimized allocation solutions for investors with varying risk profiles, helping them steer through market turbulence and capture long-term value.

Data Sources: Bloomberg, AQUMON Limited

About us

AQUMON is a Hong Kong based award-winning financial technology company. Our mission is to leverage AI and algorithm to make next-generation investment services affordable, transparent and accessible to both institutional clients and the general public. Through its proprietary algorithms and scalable, technical infrastructure, AQUMON’s automated platform empowers millions to invest and maximize their returns. AQUMON has partnered with more than 50 financial institutions in Asia.

The brand is held under Magnum Research Limited and is licensed with Type 1, 4 and 9 under the Securities and Futures Commission (SFC) of Hong Kong. CE Number: BJU619.

Disclaimer

Viewers should note that the views and opinions expressed in this material do not necessarily represent those of Magnum Research Group and its founders and employees. Magnum Research Group does not provide any representation or warranty, whether express or implied in the material, in relation to the accuracy, completeness or reliability of the information contained herein nor is it intended to be a complete statement or summary of the financial markets or developments referred to in this material. This material is presented solely for informational and educational purposes and has not been prepared with regard to the specific investment objectives, financial situation or particular needs of any specific recipient. Viewers should not construe the contents of this material as legal, tax, accounting, regulatory or other specialist of technical advice or services or investment advice or a personal recommendation. It should not be regarded by viewers as a substitute for the exercise of their own judgement. Viewers should always seek expert advice to aid decision on whether or not to use the product presented in the marketing material. This material does not constitute a solicitation, offer, or invitation to any person to invest in the intellectual property products of Magnum Research Group, nor does it constitute a solicitation, offer, or invitation to any person who resides in the jurisdiction where the local securities law prohibits such offer. Investment involves risk. The value of investments and its returns may go up and down and cannot be guaranteed. Investors may not be able to recover the original investment amount. Changes in exchange rates may also result in an increase or decrease in the value of investments. Any investment performance information presented is for demonstration purposes only and is no indication of future returns. Any opinions expressed in this material may differ or be contrary to opinions expressed by other business areas or groups of Magnum Research Limited and has not been updated. Neither Magnum Research Limited nor any of its founders, directors, officers, employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of this material or reliance upon any information contained herein.