Retail Investors Drive Markets into Positive Territory

Written by Ken on 2020-06-09

Global financial markets continue to rally strongly into June on the back of continued positive news. Last week the US’ S&P 500 Index was +4.91% and -1.14% year to date. Locally the Heng Seng Index rebounded strongly on the back of economic recovery in the Asia Pacafic region +7.88% last week and -12.13% year to date.

AQUMON’s diversified ETF portfolios were +0.00% (defensive) to +4.75% (aggressive) last week and +1.35% (defensive) to -2.55% (aggressive) year to date. Last week markets continued to be driven by risk assets across all regions with US small caps and emerging markets (EM) leading the way +7.94 and +7.79%. Sector wise energy stocks had a strong rebound + 15.69%. Riskier bonds such as emerging markets and high yield were up +2.26% and +2.88%.

This week our focus will be on the impact of US retail investors in the recent rally, reading deeper in the surprisingly positive US jobs report and also outline some positive drivers for Hong Kong markets in the next few months.

Retail investors continue to drive markets into positive territory.

With the Federal Reserve (Fed) reducing interest rates to zero, offering ‘unlimited’ quantitative easing and outright purchasing assets such as junk (high yield) bonds coupled with large scale surge in retail investor support has kept markets rallying from late-March into June. As of Tuesday the US S&P 500 Index is +0.05% year to date and rallied a whopping +35.47% since market bottom on March 16th. If you remember, the S&P Index was -26.14% year to date on March 16th. What a turnaround! This only took a surprising 84 days for markets to rebound completely back into the black year to date.

A good portion of this can be accredited to the huge wave of novice investors coming into the markets while experienced institutional investors mainly stayed sidelined. So why did these new investors flock to markets? Many industry analyst theorize it is a mixture of the following:

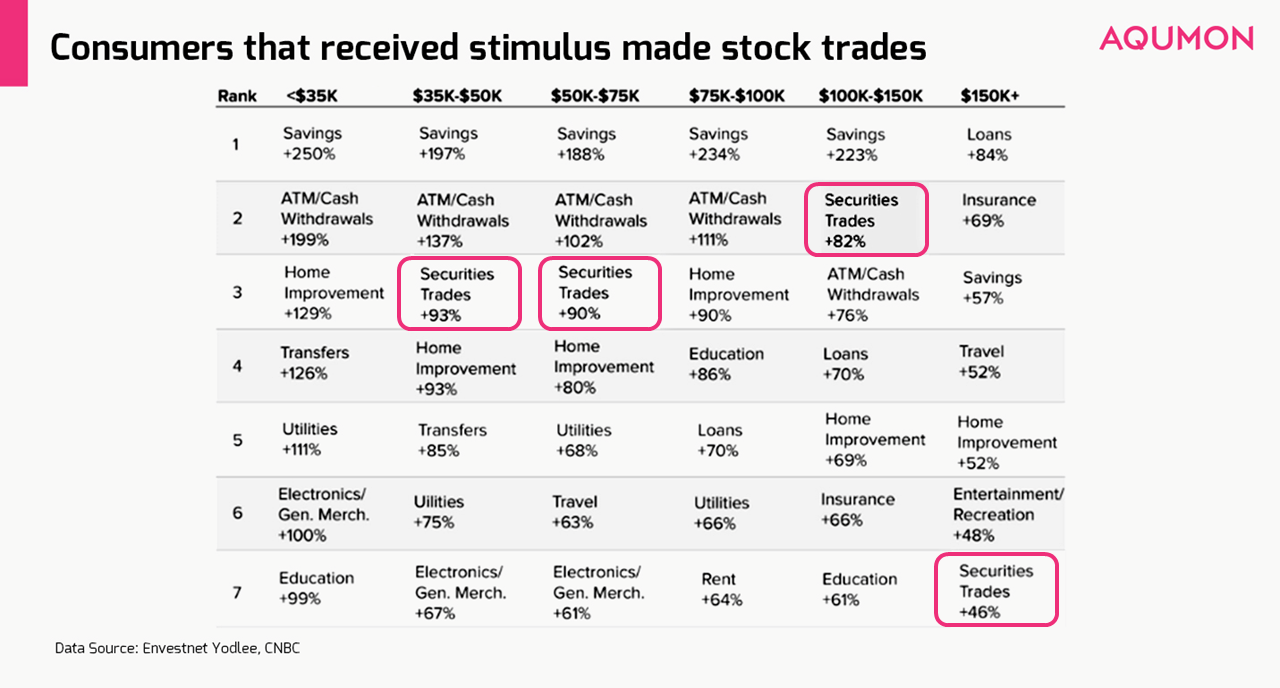

1) Americans ‘punting’ their US$1,200 (~HK$9,300) stimulus cheques: If you remember we pointed out 2 weeks ago investing into the market was one of the most common ways for Americans to spend their US$1,200 (~HK$9,300) stimulus check for almost all income brackets:

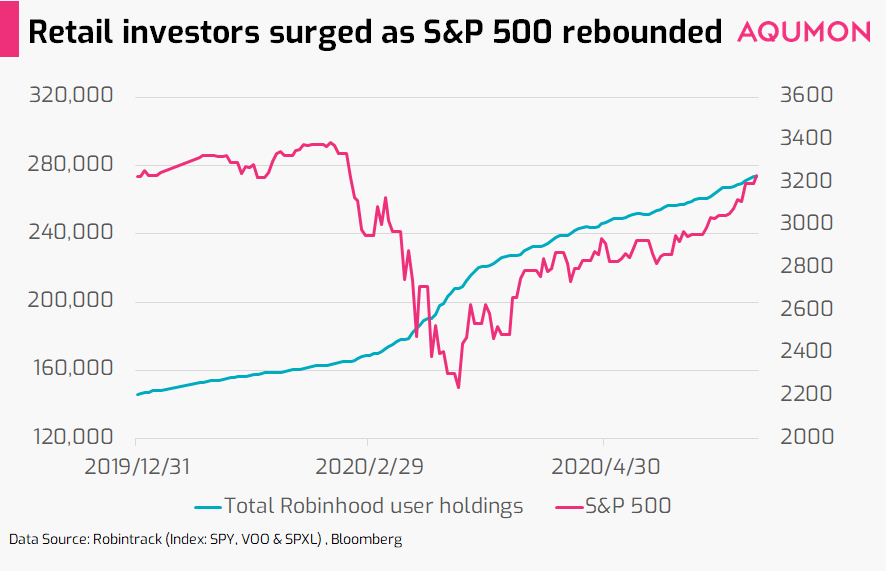

2) Availability of zero to low commission trading along with cheap leverage: In 2019 many large US brokerages pivoted to a zero commissions fee model along with offering cheap leverage (ability to invest using borrowed money in theory to amplify your returns) for investors. Taking openly available data from US retail investment app Robinhood we can see their increase in user stock holdings in both the S&P 500 ETF along with highly leveraged (riskier) S&P 500 ETFs perfectly correlates against the recent V shape recovery of the actual S&P 500 Index:

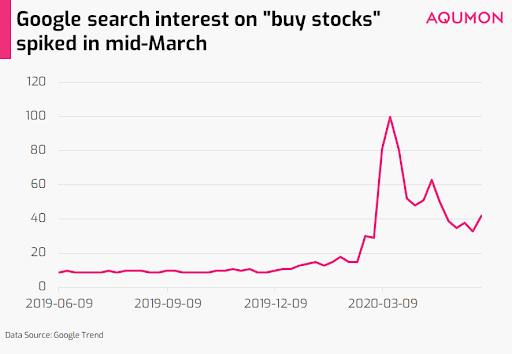

3) Lack of sports, gambling and entertainment options: With casinos and major sports on lockdown due to COVID-19 many Americans starting in mid to late March turned to find ‘entertainment’ in the stock market which would suggest why Google searches for “buy stocks” spiked (along with increased chatter on buying opportunity from this historical selloff):

This would anecdotally explain why markets continue to grind up amidst consistent negative fundamental data because a novice investor may rarely look at valuations, economic data or balance sheets when making their investment decisions.

Why do we mention this? Because as smart investors we need to be aware that the effect of these stimulus cheques will run out (thereby reducing market liquidity) and entertainment options are becoming more readily available diverting away interest in stock markets.

If this is indeed the case, increased volatility along with more reasonably priced buying opportunities may be further ahead for those of us who missed this recent rally. For the time being the market should still continue to find support and a boost from both central bank stimulus and investors.

Surprise US jobs report gained 2.5 million jobs in May but details show a bit of concern.

Financial markets late last week also surged on the back of a positive US jobs report reading. The interesting storyline was while Wall Street economists estimated an extra 8.3 million jobs lost in May the results actually gained 2.5 million jobs resulting in a difference of 10.8 million jobs which is the largest estimate ‘miss’ in history. The 2.5 million monthly gain was also the largest single month employment gain in US record. The US unemployment rate fell to 13.3% from 14.7% instead of rising to 20%.

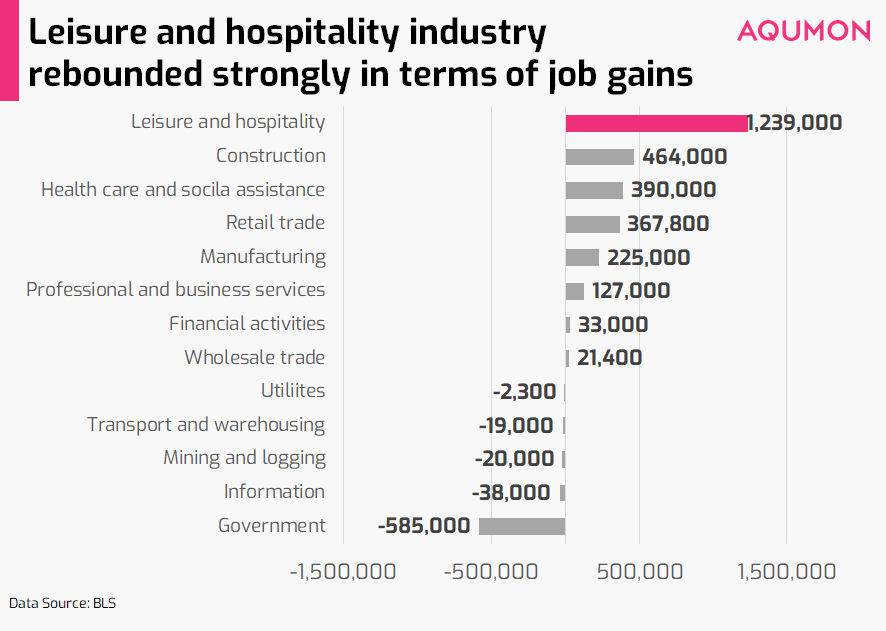

The main driver was mainly in the battered leisure and hospitality industry with 1.2 million jobs gained which is a positive sign for the US economy reopening.

Even though investors rejoiced there are 2 things investors should more closely look at:

1) The US’ Bureau of Labor (BLS) has ‘misclassified’ 4.9 million unemployed workers as employed in the jobs report: The BLS has acknowledged they have been aware of this misclassification error for 2 months now but does not correct its survey results due to appearance of manipulation. Looking at the footnotes within the US’ May jobs report you’ll find that the BLS states that workers who were not working but expected to be recalled to their jobs were classified as ‘employed but absent from work’ while they should have been classified as ‘unemployed on temporary layoff’. Why is this nuance important? The scale (4.9 million workers) is important since that means the unemployment rate should be higher than stated with April’s reading ~19.5% (actual reading 14.7%) and May’s reading ~16.1% (actual reading 13.3%). So the takeaway is the hiring situation in the US may not be as rosy as the recent turnaround seems.

2) US federal funding via the US’ Payroll Protection Program (PPP) is set to dry up in July: Within the US$510 billion (~HK$4 trillion) PPP conditions, aimed to help US businesses stay afloat, it stipulates that the maximum loan size businesses can receive is 2 ½ months of payroll and with most borrowers getting their money in April we estimate the majority of funding will be exhausted by early July. For US businesses who are tapping into the PPP for assistance if business revenues don’t improve by July then they will be faced with the tough decision of either laying off a portion of their workers or in more extreme cases closing their business. This would put increased pressure on the economy and subsequent employment readings later this summer.

Naturally, if investors choose to overlook negative readings (like they have been so far) then impact to financial markets may be muted.

Locally more support for Hong Kong markets potentially coming June and July.

Naturally, all is not negative and there are two upcoming positive factors Hong Kong investors should keep a watch out for:

1) Busy June with secondary listing initial public offerings (IPOs) by Chinese technology giants: Amid rising tensions between US and China, Chinese companies that are listed on Wall Street are encouraged to relist on the Hong Kong Stock Exchange. After Alibaba’s relisting in Hong Kong last November created the world’s largest listing in 2019 in the pipeline for June is NetEase, one of China’s largest gaming companies, is set to begin trading June 11th. Immediately behind is Chinese e-commerce giant JD.com set to trade on June 18th. Combined both companies are set to raise local proceeds of US$5 billion (~HK$38.8 billion). The increased interest driven by local, southbound (from mainland China) and foreign investors should provide an additional boost for the Hang Seng Index in June.

2) HK$10,000 cash handout coming as early as July: Hong Kong Financial Secretary Paul Chan announced Monday that eligible Hong Kong permanent residents will be able to receive the first payments for the HK$10,000 cash handout as early as July 8th. As per Chan most eligible residents should receive their handout by the end of August. The total size of the cash handout is estimated to be HK$71 billion.

Remember what we said above about American’s investing their stimulus cheques into the market? We feel it is highly possible that a sizable portion of Hong Kong citizens will follow a similar stock investing pattern come July providing some added uplift for local financial markets.

The two positive factors combined could potentially deliver up to an additional HK$100+ billion of liquidity for Hong Kong markets.

If you have any questions please don’t hesitate to reach out to us at AQUMON. We’re always happy to help. Thank you again for your continued support for AQUMON, stay safe outside and happy investing!

About us

As a leading startup in the FinTech space, AQUMON aims to make sophisticated investment advice cost-effective, transparent and accessible to both institutional and retail markets, via the adoptions of scalable technology platforms and automated investment algorithms.

AQUMON’s parent company Magnum Research Limited is licensed with Type 1, 4 and 9 under the Securities and Futures Commission of Hong Kong. In 2017, AQUMON became the first independent Robo Advisor to be accredited by the SFC.

AQUMON’s investors include Alibaba Entrepreneurs Fund, Bank of China International and HKUST.

Disclaimer

Viewers should note that the views and opinions expressed in this material do not necessarily represent those of Magnum Research Group and its founders and employees. Magnum Research Group does not provide any representation or warranty, whether express or implied in the material, in relation to the accuracy, completeness or reliability of the information contained herein nor is it intended to be a complete statement or summary of the financial markets or developments referred to in this material. This material is presented solely for informational and educational purposes and has not been prepared with regard to the specific investment objectives, financial situation or particular needs of any specific recipient. Viewers should not construe the contents of this material as legal, tax, accounting, regulatory or other specialist of technical advice or services or investment advice or a personal recommendation. It should not be regarded by viewers as a substitute for the exercise of their own judgement. Viewers should always seek expert advice to aid decision on whether or not to use the product presented in the marketing material. This material does not constitute a solicitation, offer, or invitation to any person to invest in the intellectual property products of Magnum Research Group, nor does it constitute a solicitation, offer, or invitation to any person who resides in the jurisdiction where the local securities law prohibits such offer. Investment involves risk. The value of investments and its returns may go up and down and cannot be guaranteed. Investors may not be able to recover the original investment amount. Changes in exchange rates may also result in an increase or decrease in the value of investments. Any investment performance information presented is for demonstration purposes only and is no indication of future returns. Any opinions expressed in this material may differ or be contrary to opinions expressed by other business areas or groups of Magnum Research Limited and has not been updated. Neither Magnum Research Limited nor any of its founders, directors, officers, employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of this material or reliance upon any information contained herein.