The Challenges and Opportunities of WealthTech Transformation

Written by AQUMON Team on 2022-03-31

It would be quite the understatement to say that the wealth management industry is in the midst of significant change. Between the Great Wealth Transfer and digital transformation set to take place in the coming years, the entire industry is being confronted with systemic changes that are transforming how businesses operate in a post-pandemic epoch. Driven by both structural trends and lockdowns, investors and their advisors now expect seamless experiences that are putting pressure on the traditional business models employed by wealth managers.

Much of the reason the wealth management industry has been slow in adopting digital transformation lies in the nature of the work that they do. Wealth managers are built upon human interaction and personal relationships, qualities that on first glance appear to be at odds with technology. When paired with the confidence most managers have in their ability to achieve ‘alpha’ returns for their clients, impersonal robo-advisors or mobile apps begin to take on a relatively lackluster appeal when compared to an experienced wealth manager from the likes of Morgan Stanley or UBS.

To this end, private wealth managers and investment managers altogether tend to show the greatest gaps in their digital adoption. This may be due, in part, to the belief that they cannot automate their investors’ complex financial situations without sacrificing the quality of service the industry has become known for.

But with the advent of COVID-19, wealth managers were faced with the harsh reality of their weaknesses pertaining to satisfying the digital needs of their customers. As emails and phone calls became substitutes to face-to-face communication during lockdowns, it became apparent that firms and their advisors needed to adopt a proactive approach to client engagement and demonstrate that they are able to add real value to the investment equation. One way they are able to do so is by using digital wealth tools.

How is digitisation becoming the new normal in wealth management?

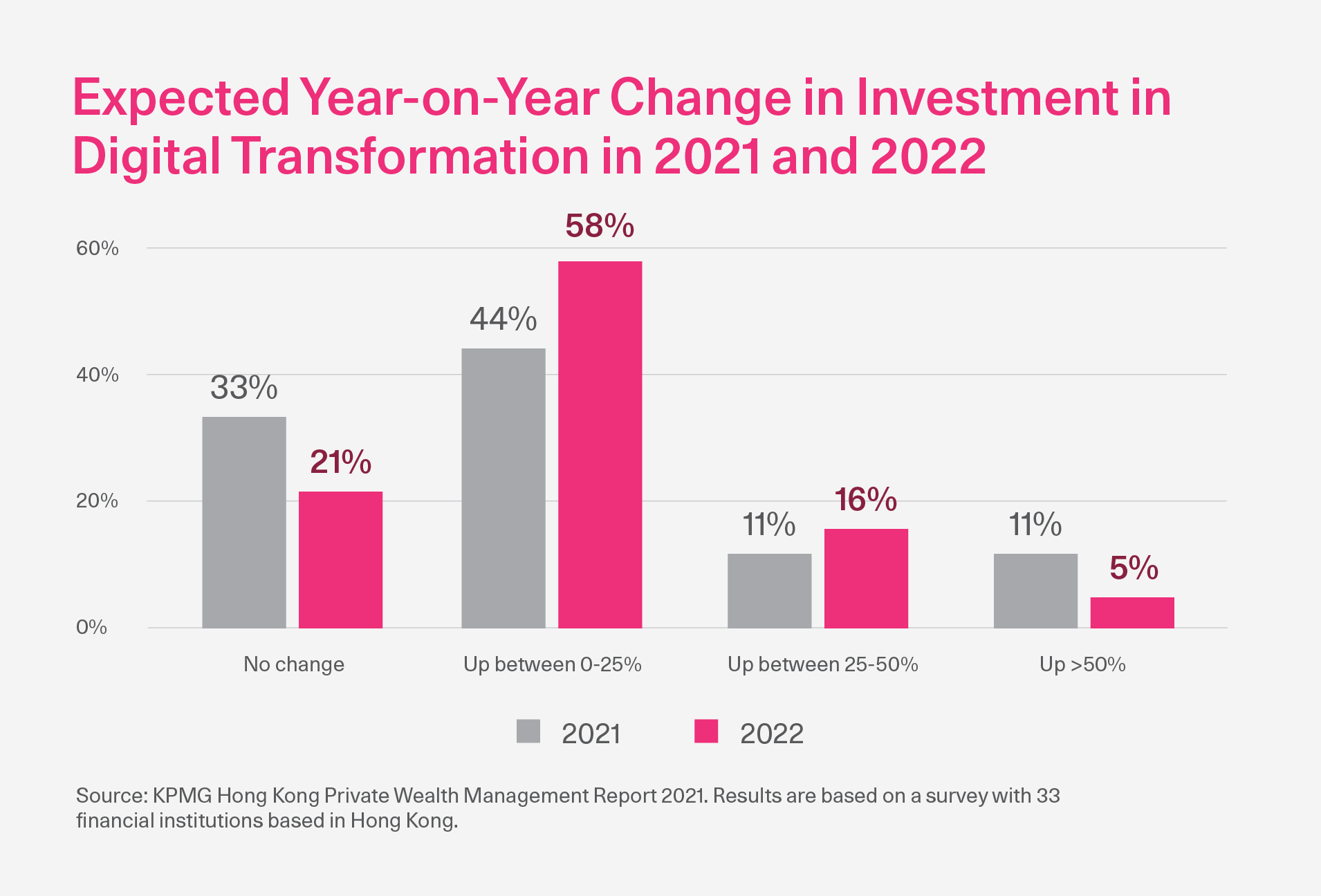

The ever changing landscape of wealth management, which has been made even more complex by the pandemic, calls for wealth management firms to deliver omnichannel investing experiences that are more personalised and digitised than ever before. A recent study on the APAC wealth management industry by KPMG revealed several drivers for digital transformation and the expectations wealth managers have to meet:

1. Shift to digital:

Next-generation investors, especially Gen-Y and Gen-Z investors, want tailored multi-channel offerings which include digital access to their accounts and 24/7 monitoring of their portfolios. These platforms are expected to be mobile and web-based.

2. Democratisation:

Clients want investment alternatives that are personalised to their financial planning needs as well as more accessible for their modern lifestyle. Providing these services in digital format helps to meet these needs.

3. Lower, more transparent fees:

Gen-Y and Gen-Z investors are fee-conscious investors compared to their older counterparts. Next-gen investors believe that a transparent wealth manager acts in their best interests.

4. Competitors delivering better customer experiences:

Robo-advisors and FinTechs are better prepared to offer products and services that match the digital expectations of today’s tech-enabled clients.

Challenges and Risks Facing Slow Adopters

Thus far, wealth management firms have been doing a good job staying afloat despite the systemic changes that are taking place in the industry. However, it is important to note that the average client profile for wealth managers is changing rapidly. As firms need to bring in new business, they will have to consider what is required to earn and retain new clients.

1. The Great Wealth Transfer:

Credit Suisse estimates that wealth valued at nearly US$8.6 trillion* will be transferred between generations from now until 2029, and this figure applies to APAC alone. Millenials in particular are now transitioning into a period of their lives in which they have significant investable assets predominantly inherited from their Baby-Boomer parents. Wealth management firms must start understanding the wants and needs of this new generation of clients.

Compared to their parents, Millennials are digital natives who are more involved in their investing. They prefer to do their own research and curate investment plans tailored to their specific needs, so earning their trust and business will take more effort.

2. Too Little, Too Late:

Firms that believe they can wait until tech-savvy Millennials are ready for their services will be left in the shadows by more agile FinTech firms. These investors value convenience in the form of digitised product and service offerings.

3. Pandemic Impacts:

Perhaps one of the most surprising developments in the industry is the viability of non-traditional business models within finance. Not only is it possible to personalise investment advice for customers through digital means like a robo-advisor or a mobile app, but investors have been quick to demonstrate their preference for such digital digital channels. Firms who have invested heavily in digitisation pre-pandemic were able to transition smoothly towards omnichannel distribution formats.

4. Intensifying Competition:

Wealth management firms are facing competition from FinTechs aiming for their market share. Traditional firms have been able to allay competitive concerns by emphasizing their customer awareness compared to their digital counterparts. So far, traditional firms have been able to use this competitive advantage to support their higher fees, but this position will likely change.

Firms that acquire customers solely through the lens of wealth status might see that some high-income clients may not be as profitable as originally thought. In Hong Kong alone, 94.4% of the affluent population (or 4.23m people) are considered to be mass affluent (holding liquid assets between US$50k and US$1m), while only 5.6% (or 0.27m) of the affluent segment is considered HNW or UHNW^. With this perspective, firms that accept clients based on net worth may be losing out on revenue.

How Firms are Addressing Challenges?

Wealth managers late in the digitisation game are addressing the aforementioned challenges by adopting a client-centric approach. But doing so requires a holistic understanding of the customer and the adoption of tools to anticipate their needs and wants.

This strategy challenges an advisor’s role to a certain degree. Advisors are still available for personalised support and to resolve complex issues that necessitates human touch. Implementing digital self-service, wealth management advisor portals, and automation actually boosts advisors’ efficiency and frees them up to be with clients when they are needed the most.

Make Digitisation a Reality

Digitised solutions are needed by wealth management firms to fill the void between traditional business models and the changing demands of customers who want digital services. If you are part of a firm that is starting to develop and implement a digital strategy, it is important to prioritise your needs based on your desired business impact.

Accelerate your digital transformation and start seeing results sooner through a software platform like AQUMON. AQUMON provides digital solutions designed to help improve efficiency, effectiveness and create a seamless digital experience for your clients. Our solutions empower advisors and clients through unparalleled data, flexible technology, streamlined workflow activities, and personalized digital capabilities.

Interested in learning more? Schedule a demo session with our Institutional Services Team to digitally transform your business.

Sources:

^Source: GlobalData Banking and Payments Intelligence Centre

About us

AQUMON is a Hong Kong based award-winning financial technology company. Our mission is to leverage smart technology to make next-generation investment services affordable, transparent and accessible to both institutional clients and the general public. Through its proprietary algorithms and scalable, technical infrastructure, AQUMON’s automated platform empowers anyone to invest and maximise their returns. AQUMON has partnered with more than 100 financial institutions in Hong Kong and beyond, including AIA, CMB Wing Lung Bank, ChinaAMC, and Guangzhou Rural Commercial Bank. Hong Kong University of Science and Technology, the Alibaba Entrepreneurs Fund, affiliate of BOC International Holdings Limited, Zheng He Capital Management and Cyberport are among AQUMON's investors.

The brand is held under Magnum Research Limited and is licensed with Type 1, 4 and 9 under the Securities and Futures Commission (SFC) of Hong Kong. AQUMON is also licensed by the U.S. Securities and Exchange Commission (SEC) and the Asset Management Association of China (AMAC).

Disclaimer

Viewers should note that the views and opinions expressed in this material do not necessarily represent those of Magnum Research Group and its founders and employees. Magnum Research Group does not provide any representation or warranty, whether express or implied in the material, in relation to the accuracy, completeness or reliability of the information contained herein nor is it intended to be a complete statement or summary of the financial markets or developments referred to in this material. This material is presented solely for informational and educational purposes and has not been prepared with regard to the specific investment objectives, financial situation or particular needs of any specific recipient. Viewers should not construe the contents of this material as legal, tax, accounting, regulatory or other specialist of technical advice or services or investment advice or a personal recommendation. It should not be regarded by viewers as a substitute for the exercise of their own judgement. Viewers should always seek expert advice to aid decision on whether or not to use the product presented in the marketing material. This material does not constitute a solicitation, offer, or invitation to any person to invest in the intellectual property products of Magnum Research Group, nor does it constitute a solicitation, offer, or invitation to any person who resides in the jurisdiction where the local securities law prohibits such offer. Investment involves risk. The value of investments and its returns may go up and down and cannot be guaranteed. Investors may not be able to recover the original investment amount. Changes in exchange rates may also result in an increase or decrease in the value of investments. Any investment performance information presented is for demonstration purposes only and is no indication of future returns. Any opinions expressed in this material may differ or be contrary to opinions expressed by other business areas or groups of Magnum Research Limited and has not been updated. Neither Magnum Research Limited nor any of its founders, directors, officers, employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of this material or reliance upon any information contained herein.