2022 Q3 Market Insights and Portfolio Performance Updates

Written by AQUMON Team on 2022-11-24

2022 Q3 Market Insights and Portfolio Performance Updates

Looking back to the third quarter of 2022, continued high inflation and interest rate hikes, the energy shortage crisis in Europe, repeated outbreaks of COVID-19 across China, and the ongoing escalation of the Russia-Ukraine conflict increased market risk and instability, making it another difficult period for investors.

How will the AQUMON portfolio perform in such a volatile market? Can global asset allocation perform consistently and consistently? What can we expect from financial markets in the upcoming fourth quarter? Stay tuned.

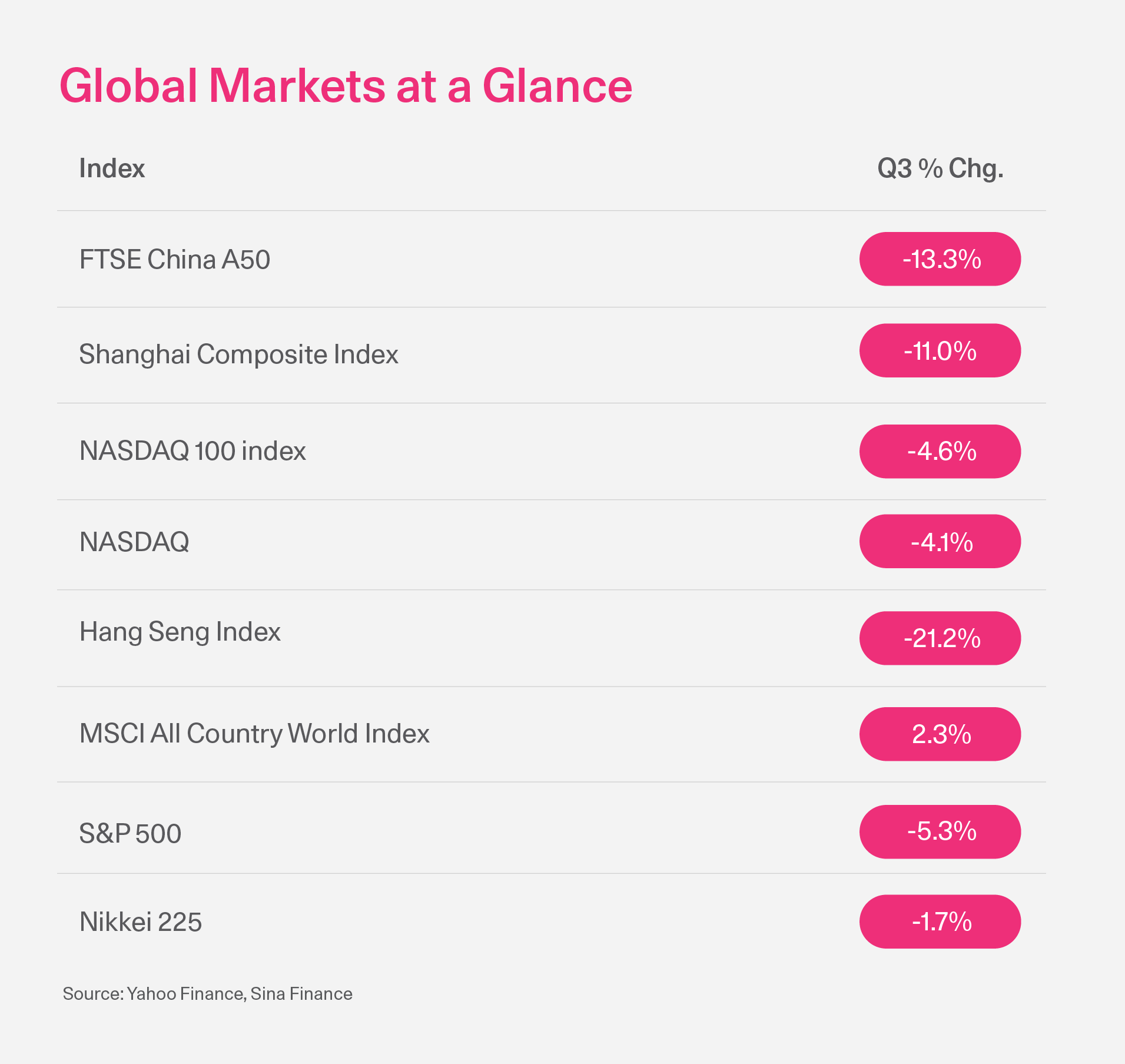

2022 Q3 Global Financial Markets Key Highlights

The third quarter of 2022 continued the downward economic trend seen in the second quarter of 2022, with markets in turmoil and key events as follows:

-

The S&P 500 fell 4.9 percent in the third quarter and 23.9 percent so far this year as financial market adjustments intensified after the Fed raised rates by 75 basis points at its September meeting

-

The outlook for the European market economy continues to deteriorate, the negative impact of the ongoing conflict between Russia and Ukraine continues to intensify, and the energy shortage in Europe is further amplified

-

The dollar continued to strengthen in the third quarter, with Yahoo Finance reporting that the dollar has gained more than 17 percent in 2022, while the Japanese yen, euro and pound have all depreciated and national exchange rates have hit record lows

-

The mainland of China is firmly committed to the "zero-COVID policy". Due to the impact of the epidemic, the mainland's economic growth has slowed down

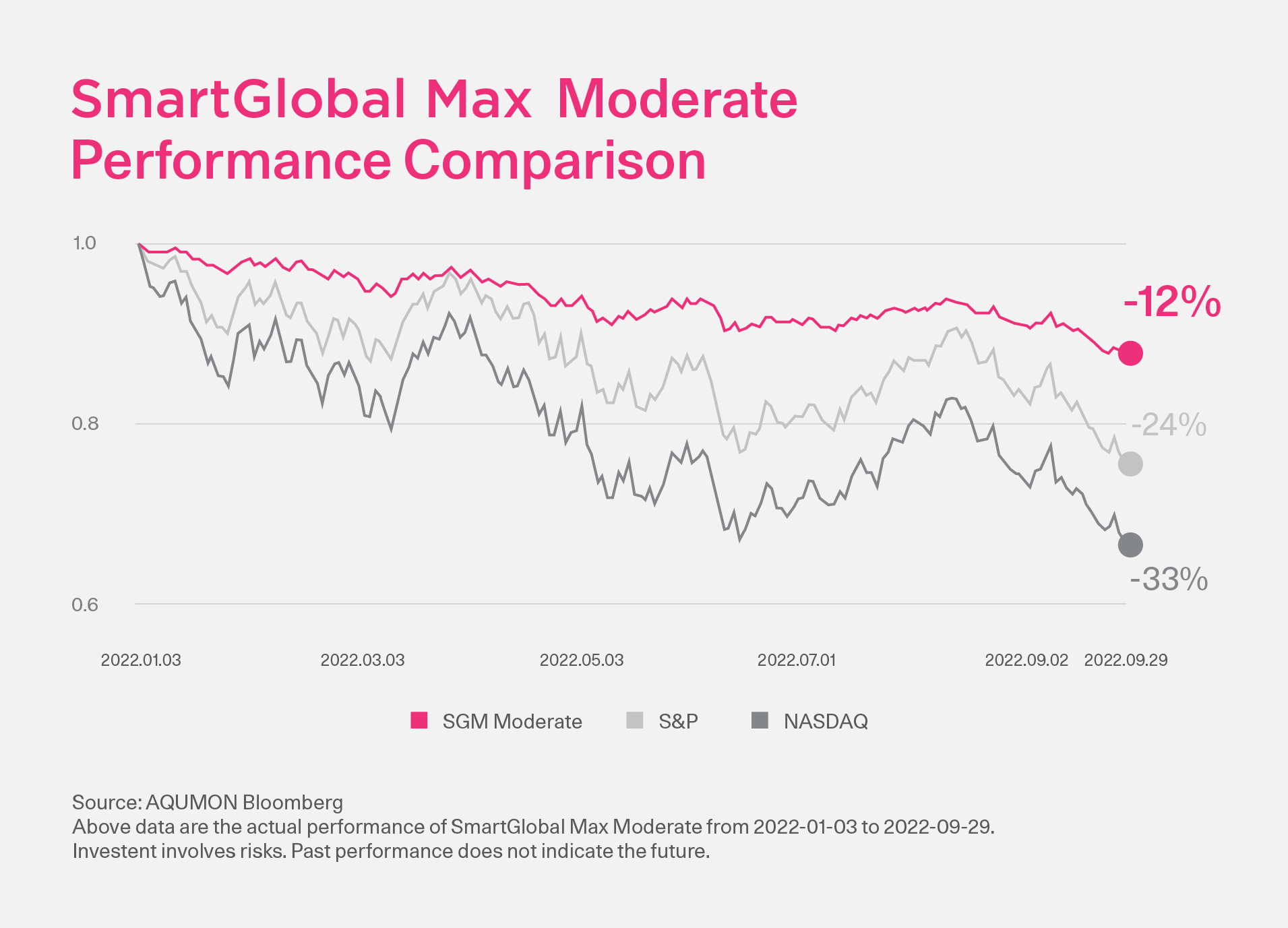

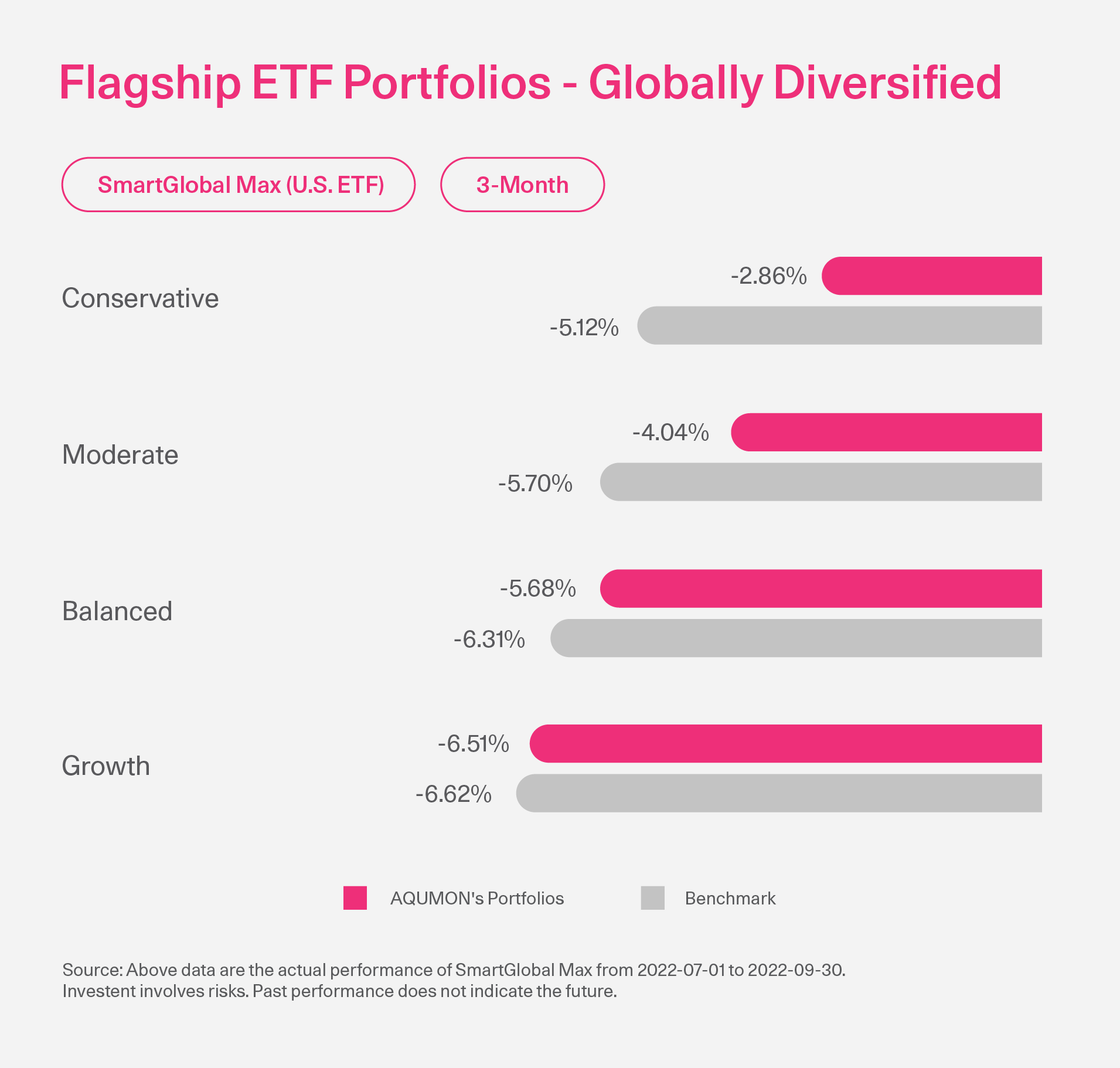

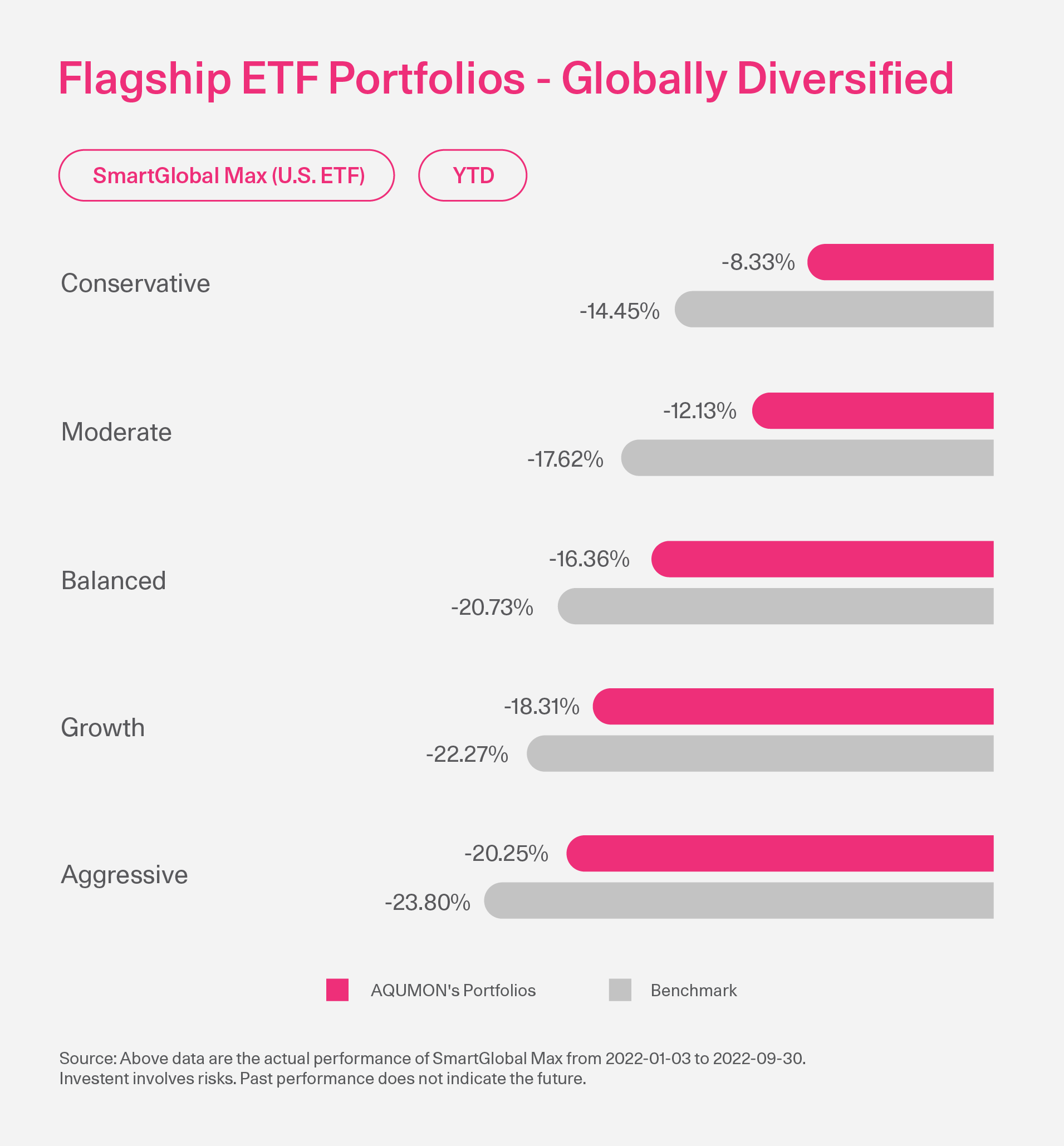

How Did Aqumon’s Portfolios Perform?

-

SGM Moderate

Actual performance of the flagship ETF asset allocation portfolio compared to the benchmark in the first three quarters of 2022. AQUMON's unique global asset allocation strategy has outperformed the benchmark in terms of returns, maximizing benefits for investors and demonstrating strong resilience to market volatility.

Will It Be Better in 2022 Q4?

-

The macro core factor for the US going forward is inflation. We expect the Fed to keep raising rates based on inflation until core CPI peaks in the third quarter of 2023. In the worst-case scenario, the Fed funds rate could reach around 5%

-

With the supply chain crisis and labor shortage in the US in the wake of the global pandemic, combined with the impact of the Russia-Ukraine conflict on energy and food prices this year, we expect the Fed to quickly raise interest rates to the maximum level that the US government can afford, and stay high for an extended period

-

There is a high probability that the three indexes will wear out after the third quarter of 2022. The main reason is that the Federal Reserve will continue to raise interest rates and maintain the interest rate above 4.5% until after the third quarter of 2022, which will greatly reduce the liquidity of the stock market

-

Commodity prices are likely to continue to fall in the future as energy prices fall and the US Federal Reserve continues to raise interest rates. The ongoing escalation of the conflict between Russia and Ukraine and the impact of the new COVID-19 outbreak in mainland China on the global supply chain are highly uncertain

-

The Chinese mainland has adhered to the policy of dynamic elimination of epidemic prevention, and the new wave of COVID-19 may continue to have a certain impact on the market

How Should Investors Adjust Their Asset Allocation?

Given that uncertainty will continue in the second half of 2022, investors should keep their defensive positioning by focusing on stable return vehicles. The best way to weather turbulence is through diversification.

- Drive up diversification on different aspects of the portfolio in the asset class, geographic location & sector.

- Remain relatively conservative while finding ways to enhance a portfolio's Sharpe ratio*.

- Place more weighting on Chinese or Chinese-linked assets, which will benefit from low valuations, a recovering economy, and supportive fiscal and monetary policy while other major global economies continue fiscal and monetary policy tightening.

*One of the widely used methods for calculating risk-adjusted returns. The higher the ratio, the greater the investment return relative to the amount of risk taken, and thus, the better the investment.

Hyper-Personalised Investment Solutions-AQUMON Bespoke

A multi-asset portfolio with global exposure carrying a dynamic allocation pertaining to underlying economic growth could potentially offset current market turmoil, if a systematic approach is there to afford the right asset mix plus proper ongoing refinements. Schedule a free consultation with us to learn more about AQUMON's investment products and market-adapting solutions.

You may also contact us via 2155 2816, WhatsApp, or email bespoke@aqumon.com

About us

AQUMON is a Hong Kong based award-winning financial technology company. Our mission is to leverage smart technology to make next-generation investment services affordable, transparent and accessible to both institutional clients and the general public. Through its proprietary algorithms and scalable, technical infrastructure, AQUMON’s automated platform empowers anyone to invest and maximize their returns. AQUMON has partnered with more than 100 financial institutions in Hong Kong and beyond, including AIA, CMB Wing Lung Bank, ChinaAMC, and Guangzhou Rural Commercial Bank. Hong Kong University of Science and Technology, the Alibaba Entrepreneurs Fund, affiliate of BOC International Holdings Limited, Zheng He Capital Management and Cyberport are among AQUMON's investors.

The brand is held under Magnum Research Limited and is licensed with Type 1, 4 and 9 under the Securities and Futures Commission (SFC) of Hong Kong. AQUMON is also licensed by the U.S. Securities and Exchange Commission (SEC) and the Asset Management Association of China (AMAC).

Disclaimer

Viewers should note that the views and opinions expressed in this material do not necessarily represent those of Magnum Research Group and its founders and employees. Magnum Research Group does not provide any representation or warranty, whether express or implied in the material, in relation to the accuracy, completeness or reliability of the information contained herein nor is it intended to be a complete statement or summary of the financial markets or developments referred to in this material. This material is presented solely for informational and educational purposes and has not been prepared with regard to the specific investment objectives, financial situation or particular needs of any specific recipient. Viewers should not construe the contents of this material as legal, tax, accounting, regulatory or other specialist of technical advice or services or investment advice or a personal recommendation. It should not be regarded by viewers as a substitute for the exercise of their own judgement. Viewers should always seek expert advice to aid decision on whether or not to use the product presented in the marketing material. This material does not constitute a solicitation, offer, or invitation to any person to invest in the intellectual property products of Magnum Research Group, nor does it constitute a solicitation, offer, or invitation to any person who resides in the jurisdiction where the local securities law prohibits such offer. Investment involves risk. The value of investments and its returns may go up and down and cannot be guaranteed. Investors may not be able to recover the original investment amount. Changes in exchange rates may also result in an increase or decrease in the value of investments. Any investment performance information presented is for demonstration purposes only and is no indication of future returns. Any opinions expressed in this material may differ or be contrary to opinions expressed by other business areas or groups of Magnum Research Limited and has not been updated. Neither Magnum Research Limited nor any of its founders, directors, officers, employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of this material or reliance upon any information contained herein.